This article looks at what top lenders are doing to mitigate the effects of appraiser shortages with the UAD 3.6 deadline approaching. It provides three steps that bank, credit union and nonbank lenders – agency and non-agency – can take to avoid disruption to their business operations and borrowers.

On November 2, 2026 use of the Uniform Appraisal Dataset (UAD) 3.6 becomes mandatory for loans delivered to Fannie Mae and Freddie Mac. This transition replaces legacy appraisal forms with a structured, standardized dataset aligned to the new Uniform Property Data (UPD) standard for interior/exterior inspections.

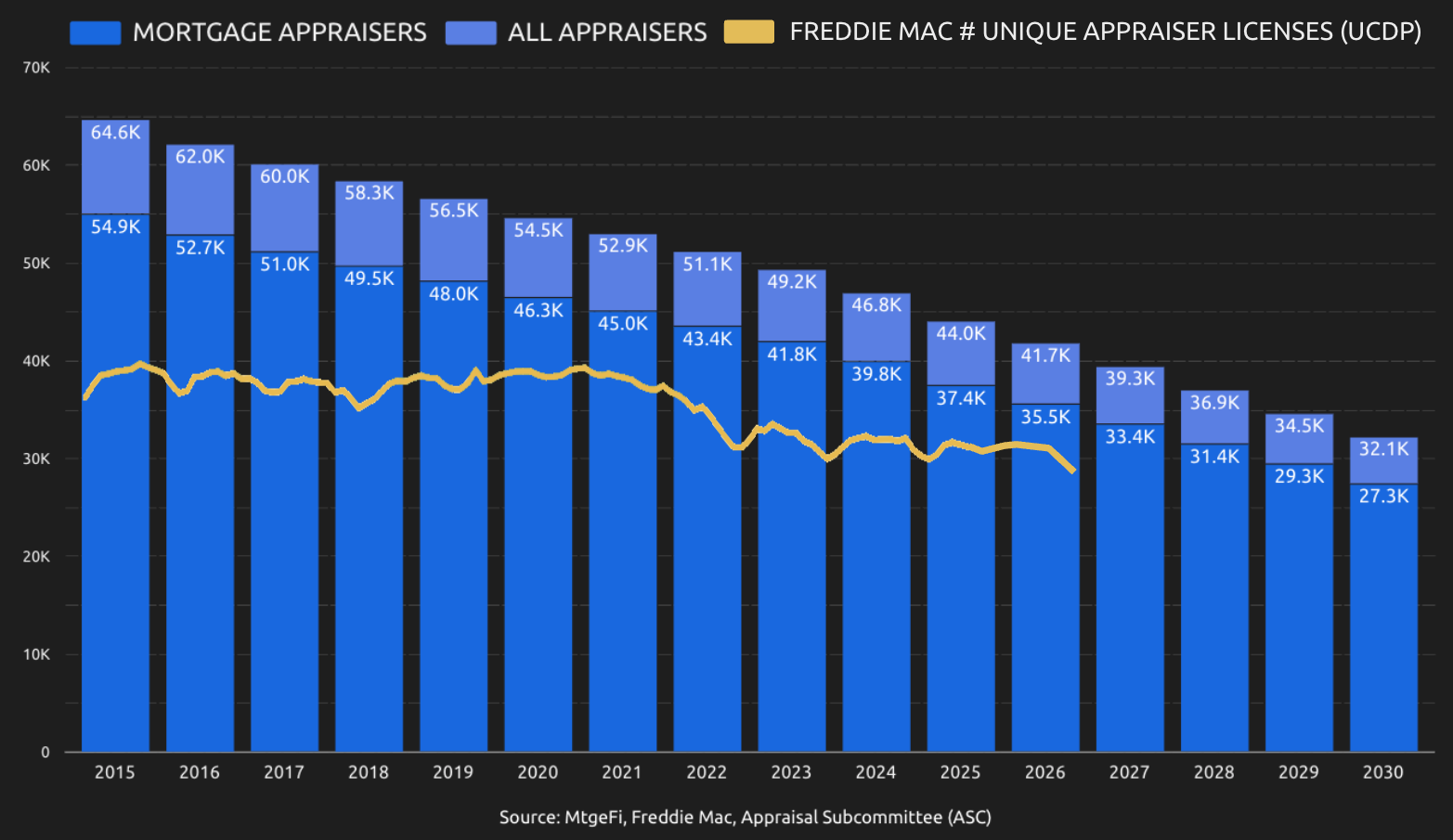

Industry feedback suggests that 10–15% of appraisers may retire from the profession rather than adapt to UAD 3.6. Privately, many in the industry believe the impact could be as high as 25%, and disproportionately impact markets that already face challenges meeting demand today.

This is occurring within the context of a decades-long decline in active appraisers: In 2025 a further 2,456 appraisers did not renew their licenses, taking the estimated total active to 37,359. By comparison, the AQB reports a total of 551 appraisers – 191 licensed residential and 360 certified residential passed exams for the first time in 2025. With these licenses included, the annual decrease is 3,000+ appraisers.

Why is UAD 3.6 Being Implemented?

UAD 3.6 is a Fannie Mae and Freddie Mac initiative to modernize appraisal reporting by replacing static forms with a structured XML dataset.

The objective is to standardize how property and valuation data is captured, making it consistent, machine-readable, and usable across underwriting and risk management systems. UAD 3.6 supports broader property coverage, including ADUs and manufactured housing, while enabling automation in quality control and validation.

UPD and UAD 3.6 provide originators, servicers, asset managers and investors with significantly improved datasets for risk management, retention and marketing.

What Steps Are Top Lenders Taking for UAD 3.6?

Top lenders are already taking steps to mitigate the impacts of appraiser shortages.

1. Doing fewer appraisals

The most immediate step is to reduce the number of appraisals. In 2025 the top two lenders clearly prioritized closing loans without appraisals in their retail & broker channels, where they have direct control over the ordering processes.

This is the most direct lever available to lenders – 26% of GSE loans closed without appraisals via the retail and broker channels in 2025. Lenders who permit loan officers to select traditional appraisals when waivers are available will be most impacted.

GSE, FHA and VA Appraisal Waivers

Rocket Mortgage delivered 27% of their GSE loans (62,116) using appraisal waivers. This represents 19.2% of all appraisal waivers used. Similarly, UWM delivered 24% of their GSE loans (40,623) using appraisal waivers; 12.6% of all appraisal waivers used.

To put this in perspective, Rocket Mortgage (5.6%) and UWM (3.7%) combined market share of GSE loans via retail & broker channels is 9.3%, yet they were responsible for 31.8% of all loans delivered using appraisal waivers.

FHA and VA streamlined refinances do not require an appraisal. Again, top lenders like Rocket Mortgage, UWM, CrossCountry Mortgage, PennyMac, Freedom Mortgage, NewRez and Movement Mortgage’s utilization of these programs ranges from 30-60% of the loans they close that are insured by these government agencies.

GSE Inspection Based Appraisal Waivers

Rocket Mortgage and UWM were jointly responsible for originating 72.9% (28,238) of the 38,756 loans delivered to the GSEs using inspection-based appraisal waivers in 2025. The number of inspection-based appraisal waiver offers accepted has steadily increased throughout 2025, and is up significantly from a year ago, but adoption remains concentrated on top lenders.

Non-Agency Portfolio and Home Equity Lending

Under the Interagency Appraisal and Evaluation Guidelines (IAG), lenders may use an evaluation instead of an appraisal for residential real estate transactions of $400,000 or less, for commercial real estate transactions of $500,000 or less, and for business loans of $1,000,000 or less where real estate is taken as an abundance of caution. Evaluations are also permitted for renewals, refinances, or subsequent transactions where there is no new money, or no material change in market conditions or property condition.

Many lenders are using appraisals simply because they cannot locate reliable, nationwide vendors for evaluations, especially for rural markets and complex properties.

Action Items for Lenders:

Top Valuation Modernization Providers

Request more information from MtgeFi.com

2. Doing appraisals that require fewer appraisers

The next step is to reduce the number of appraisers required to complete appraisals. For lenders managing their own ‘direct-to-appraiser’ panels, this can be especially beneficial. It increases coverage without requiring additional appraisers.

Hybrid Appraisals Work for UAD 2.6 and UAD 3.6

Hybrid appraisals provide a direct solution. For the GSEs the property inspection is completed by a Data Collector using a Uniform Property Data (UPD) report. Appraisers then use the UPD report (which can include a full 3D property virtual tour), public records, MLS and other data to complete their analysis and produce an appraisal report.

This changes the unit economics of an appraisal. A traditional assignment requires the appraiser to manage the inspection, scheduling, travel, data capture, photography, borrower interaction, report creation and reporting. Now a single appraiser can complete 3-5 hybrid appraisals in a day.

Hybrid Appraisal = Traditional Appraisal = Full Appraisal = UAD 3.6 = De facto Industry Standard for GSE, Portfolio, and Non-QM Lending

The use of the term ‘full appraisal’ has become synonymous with a ‘traditional appraisal’. The GSEs, who effectively set origination underwriting industry standards in the secondary markets, have now established hybrid appraisals as a ‘full appraisal’. Fannie Mae, in particular, provides lenders with the option to use a hybrid appraisal for delivery on over 97% of loans that would previously have required a traditional appraisal.

Hybrid appraisals also offer a number of advantages to banks, credit unions and Non-QM lenders, who originate jumbo, construction, and fix-and-flip loans due to the flexibility of the UPD inspection report & data richness of UAD 3.6.

USPAP On-Site Inspection, Geographic Competence and Driving Comps

Some common misconceptions are worth addressing. First, USPAP requires geographic competency, but it does not require physical proximity. Appraisers must have, or acquire, familiarity with the market, which can be achieved through data, experience, and analysis rather than location. Second, USPAP does not require an appraiser to complete an on-site inspection. Third, under UAD 3.6 appraisers are no longer required ‘to inspect comparable sales from the exterior’, otherwise known as ‘driving comps’.

‘Direct-to-Appraiser’ Hybrid appraisals with UAD 3.6

Today, lenders can order hybrid appraisals directly from appraisers on their panel, and typically requires no changes to the current ordering processes, Loan Origination Systems (LOS) and Appraisal Management Systems (AMS). Further information is available about hybrid appraisal eligibility and hybrid appraisal adoption and benefits.

Action Items for Lenders:

3. Doing appraisals that can be completed faster

The third step is reducing the time it takes to complete the appraisal report. The combination of UPD, UAD 3.6 and new appraisal tools are dramatically reducing the time it takes to assemble, curate and upload information into an appraisal report writer.

New UAD 3.6 Appraiser Software Tools

Arguably, there has been more innovation in appraiser software in the past two years than the past two decades. Several new products have been developed in anticipation of UAD 3.6 with an overall goal to reduce manual data entry, standardize property data, and help appraisers with report analysis.

These tools typically include mobile inspection, structured data capture, floor plan and measurement technology, automated comparable and MLS data import, AI-assisted comparable selection and adjustments, and automated report writing. Others include photo analysis, quality control checks, and workflow management.

Appraisal Management Software (AMS) Optimized for UAD 3.6

Legacy AMS providers have traditionally supported the appraisal ‘place-and-chase’ workflow, and provided limited support for ordering alternative valuations and inspections. New entrants to the AMS space now offer a broader set of functionality, are more tightly integrated with Loan Origination Systems (LOS) and Point-of-Sale (POS) systems, and are designed to support a more flexible and automated workflow with minimal data entry and limited manual review steps.

Action Items for Lenders:

Recommendations

UAD 3.6 is expected to result in a reduction in the number of appraisers actively completing residential appraisals for mortgage lending.

The GSEs have worked since 2016, when appraiser shortages resulted in significant appraisal delays and fee increases, to develop modern valuations solutions for lenders as alternatives to a traditional appraisal. The solutions are available in the GSE selling guides today, but are not widely adopted.

Executive management, production, credit, or collateral policy at lending institutions should start to implement the solutions available today in the Fannie Mae and Freddie Mac Selling Guides.

Non-agency lenders should implement the full suite of alternative valuations available to them under the Interagency Appraisal and Evaluation Guidelines, and accepted by investors in the secondary markets.

Top lenders have already shifted appraisal order volume to take advantage of these solutions, and have business continuity plans in place to mitigate more severe appraiser supply shortages.